If you’ve ever felt nervous after checking your credit report, you’re not alone. Many people worry about negative items and how long they might stick around. This guide aims to clarify the timelines and help you understand what you might expect if your credit has taken a hit.

The article is especially helpful for anyone looking to repair their credit or simply curious about the credit reporting process. Understanding credit timelines might even offer a little encouragement as you plan your next financial steps.

Why Knowing Credit Report Timelines Matters

Every entry on a credit report can impact your financial life. Even small marks may affect loan applications, interest rates, or housing opportunities.

Knowing how long negative information stays on your report can help you set realistic goals for improvement. This information is essential for anyone wanting to rebuild financial stability or simply get peace of mind about their credit future.

Overview of Negative Items on Your Credit Report

Negative items are records that suggest risky financial behavior. These can range from late payments to more severe things like bankruptcies or foreclosures.

Their presence signals to lenders that you may be a higher-risk borrower. Let’s look at a few of the most common negative entries you might see:

- Late payments

- Collection accounts

- Charge-offs

- Foreclosures

- Bankruptcies

- Repossession

- Tax liens (less common in newer reports)

These items each follow their own set of rules for removal. Some may linger for nearly a decade, while others disappear a bit sooner.

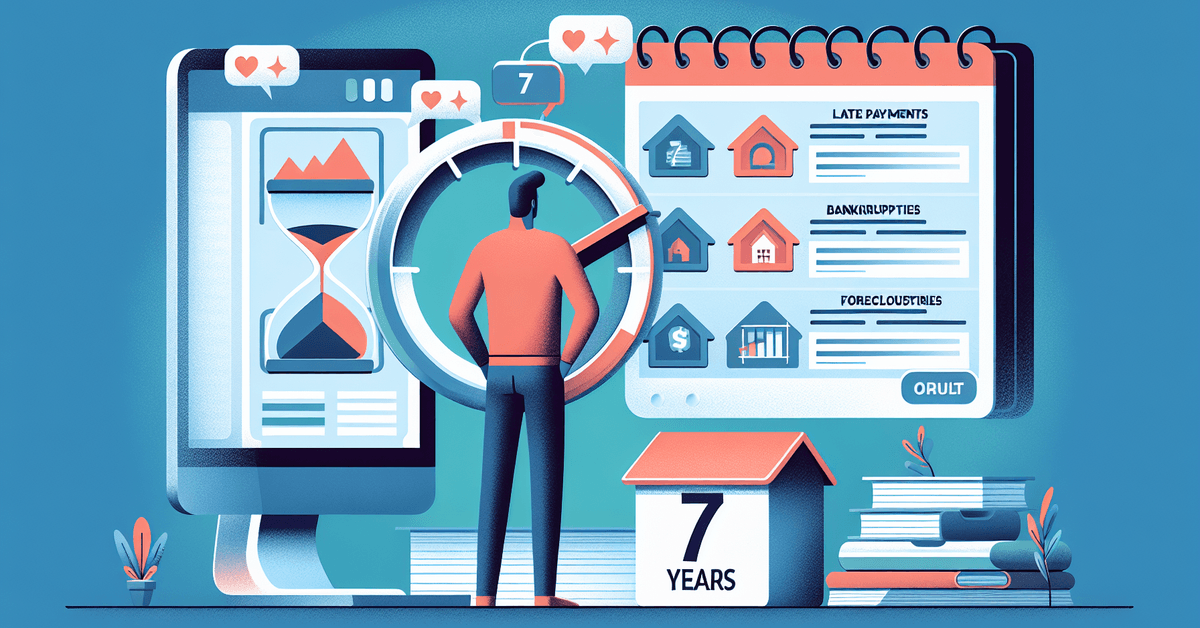

How Long Different Negative Items Stay on Your Credit Report

The time frames aren’t always simple. Each negative item has its own removal period based on type and, sometimes, local law. Here’s a breakdown of standard timelines for the most common types:

Late Payments

Late payments typically remain on your credit report for seven years from the date of the original delinquency. Even if the account is paid in full, the late mark may still be visible until that period ends. Strangely, many people think paying off the balance erases the late mark—but it doesn’t quite work that way.

Collection Accounts

Collection accounts also stay for seven years, starting from the date the original debt first became late. Whether you pay it off or it remains unpaid, the collection note generally sticks around for the full duration. Occasionally, paying may update the account as ‘paid collection,’ but the original negative status will show until expiration.

Charge-Offs

When a creditor gives up on collecting a debt, that account may be labeled as a charge-off . These, too, stick on your report for up to seven years from the time your account became past due. Paid or unpaid, the record remains until the typical timeline ends.

Bankruptcies

Bankruptcies follow their own timeline, depending on the type. Chapter 7 bankruptcies usually last for ten years. Chapter 13, where you pay back part of what you owe, usually stays for around seven years. That’s a long time, and it can be surprising just how persistent these records are.

Foreclosures

Nothing can feel quite as intimidating as a foreclosure appearing on your report. This type of negative entry generally remains for seven years. After it falls off, though, most future lenders will not see it anymore.

Repossessions

Repossessions , such as a car taken back by the lender, fall under the same seven-year rule. The date counts from the original missed payment, not the recovery date itself. A quirk that surprises some borrowers!

Tax Liens and Civil Judgments

Most tax liens have been removed from consumer credit reports due to changes in reporting rules, but if you see one, state and federal tax liens used to stay for up to seven years or longer if unpaid. Paid liens may have been removed after seven years, although this rarely applies for new reports. Civil judgments—also rare now—had similar rules.

Table: Negative Item Timelines

| Negative Item | Time on Credit Report |

|---|---|

| Late Payments | 7 years |

| Collection Accounts | 7 years |

| Charge-Offs | 7 years |

| Foreclosure | 7 years |

| Chapter 13 Bankruptcy | 7 years |

| Chapter 7 Bankruptcy | 10 years |

| Tax Liens (historical) | 7 years (varies) |

Does Paying Off Negative Items Remove Them Faster?

This is a common question. Generally, paying off a debt does not erase the negative mark before the end of its allotted time.

What it might do is update the account to ‘paid’ or ‘settled,’ which could look a little better to a future lender. Sometimes, however, creditors might agree to pay-for-delete , though this is not guaranteed and not all agencies will do it. It’s partly a matter of negotiation, not official policy.

How Accurate Are Credit Report Dates?

Credit bureaus are supposed to start the reporting period from the date of the original delinquency. However, it can be tricky, especially when debts are sold or transferred.

Sometimes, mistakes happen, and an old debt looks newer than it actually is. That’s why reviewing your credit report regularly may help. If you spot an error, you can file a dispute with the relevant bureau or creditor. The Consumer Financial Protection Bureau (CFPB) offers a useful dispute guide.

Tips for Managing Negative Credit Items

Anyone with negative items might feel discouraged. Still, small steps can help restore financial health. A few suggestions:

- Check your credit report every year, even if everything seems fine

- Dispute errors or outdated items with the credit bureaus

- Focus on current accounts to build a positive credit history

- Consider direct conversations with lenders if you’re facing hardship

It can feel overwhelming at first, but progress is possible. For more details on repairing credit, see related posts like Effective Credit Repair Tips or the official Annual Credit Report site for free checks.

Why Do Old Negative Items Matter Less Over Time?

Oddly, even though negative items stay visible for years, their impact often lessens with time. Most credit scoring models weigh recent behavior more heavily.

So, a late payment from six years ago probably won’t hit your score as hard as a recent one. Lenders may also offer more flexibility with older marks if your current financial habits are strong.

There’s really something encouraging about knowing your efforts today can slowly overshadow mistakes from years back.

Conclusion: Looking Ahead to Better Credit

Credit mistakes may not last forever, but it sometimes feels that way. Most negative items fall off after seven years—some sooner, some later—leaving room for a brighter financial future.

If your report looks less than perfect right now, remember time is usually on your side. Regular checks and a few mindful habits may help smooth the road ahead. Anyone hoping for a stronger credit score might find it’s always worth staying optimistic.

For extra guidance and tips, the resources on this site and official agencies may offer helpful next steps.