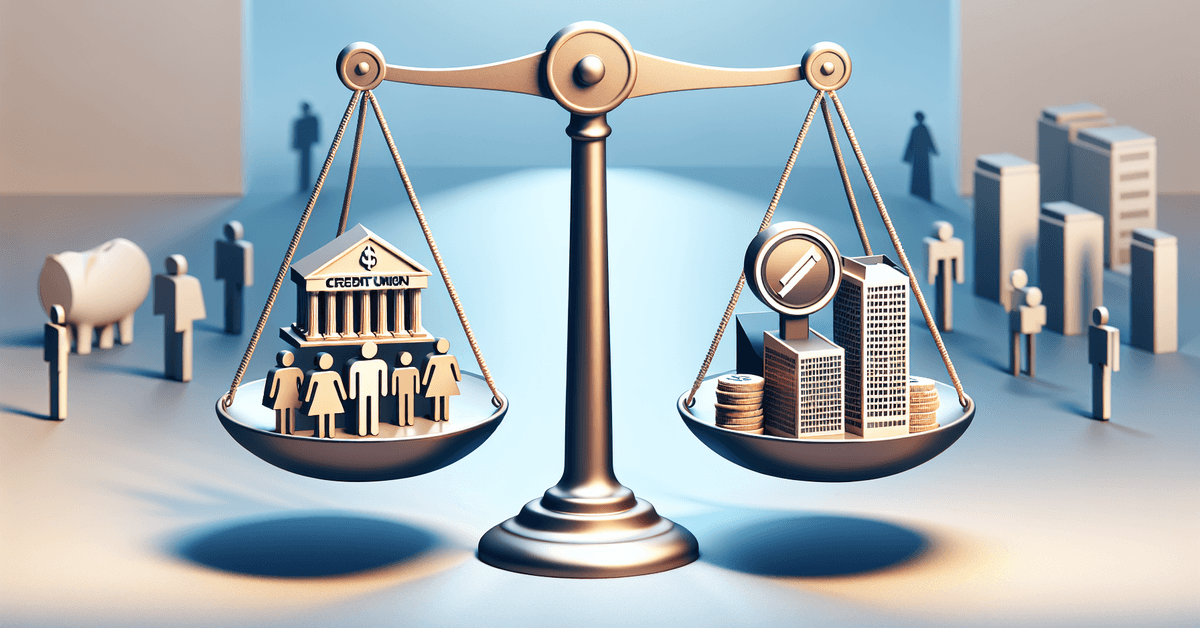

Choosing between a credit union and a traditional bank for borrowing isn’t as simple as it might seem. Both options offer benefits, but each carries its own set of trade-offs.

Many find themselves wondering which is better for their personal finance needs, particularly when it comes to securing a loan. If you’re interested in understanding the differences and making an informed decision, this article may clear some things up.

This guide is perfect for anyone curious about which financial institution might offer a better loan experience.

Whether you’re looking for a car loan, a personal loan, or even a mortgage, understanding the pros and cons of each can help you navigate the decision without regret later on.

Understanding Credit Unions and Traditional Banks

The words themselves sometimes sound interchangeable, but a credit union isn’t just another type of bank. It’s a cooperative, not-for-profit financial institution owned by its members.

On the other hand, a traditional bank runs for profit and is owned by shareholders. This fundamental difference can influence the way your loan is treated—and maybe even the rates you see.

Ownership Structure

At a credit union, the members actually have voting rights and share in the profits, often through lower fees or better loan rates. Bank profits go to investors and shareholders, not customers.

Eligibility

To join a credit union, you may need to meet specific membership requirements. This could involve your job, location, or even a family link.

Banks, in most cases, are open to everyone, which can be appealing if you want quick and easy access.

Loan Products: Comparing Options

Both offer a wide range of loans—think personal loans, mortgages, auto loans, and sometimes business loans.

But the terms, interest rates, and approval processes can differ quite a bit. For some, that difference is actually what tips the scale.

Interest Rates and Fees

Credit unions typically offer lower loan interest rates. As they aren’t aiming to increase profit margins, many members report saving noticeable sums over time.

Traditional banks usually have higher rates, but sometimes offer more promotional deals or incentives for new customers.

Flexibility

Some might say credit unions feel a bit more personal. They can occasionally tailor loan terms to individual circumstances—perhaps more than large banks typically do. That said, big banks have resources, robust online tools, and sometimes quicker approval processes.

Customer Experience and Support

Customer experience varies widely from institution to institution. Yet, a few broad patterns tend to stand out between credit unions and banks when it comes to borrowing.

Personal Interaction

Most credit unions are community-focused. You might see the same faces at your local branch each visit, and staff often know you by name.

This familiarity sometimes results in more hands-on support, especially with loan questions.

Digital Experience

Banks, owing to their size and resources, typically have more advanced digital banking platforms.

Their apps offer a broad range of features—think instant transfers, loan calculators, and even AI-powered chat support. Credit unions tend to lag slightly here, though some are catching up fast.

Loan Approval: What Matters Most?

If you’ve ever felt anxious about loan approval—well, you’re not alone. Credit standards and application requirements between the two can feel a bit different, especially when your credit score isn’t perfect.

Qualification Criteria

Credit unions sometimes consider factors beyond just credit scores, such as your overall financial habits and stability. Banks usually stick to stricter, computer-driven criteria.

Processing Times

This might sound counterintuitive, but banks’ large size lets them process certain loans faster, especially with automated approvals.

For more complex or individual requests, credit unions can be faster due to fewer layers of bureaucracy.

Safety, Insurance, and Security

It’s completely reasonable to worry about the safety of your money and personal data. Luckily, there are regulatory and security standards in place for both credit unions and banks.

Deposit Insurance

Traditional banks are insured by the FDIC up to $250,000 per account holder. Credit unions have equivalent coverage through the NCUA. In practice, this means funds are equally protected in both types of institutions.

Fraud Protection

Banks and credit unions both invest heavily in online security and fraud detection. It’s always good to review each institution’s security policies, but generally, both are considered quite safe from a consumer protection perspective.

Where Do Credit Unions and Banks Shine?

A direct comparison might help clarify things. Below is a simple table outlining some of the main points where either might have an edge:

| Factor | Credit Union | Traditional Bank |

|---|---|---|

| Interest Rates | Often lower | Varied, sometimes higher |

| Approval Flexibility | Higher, more personal | Standardized, stricter |

| Digital Tools | Improving, still trailing | Usually best-in-class |

| Branch Community | Local, community-driven | Wider branch network |

| Eligibility | Membership-based | Open to all |

Practical Tips When Choosing Where to Borrow

The choice might come down to more than numbers or policy. Consider these points when weighing your options:

- Check eligibility requirements for credit unions—sometimes joining is easier than you’d expect.

- Compare not just interest rates, but also the fees and term flexibility offered by each lender.

- Read reviews or talk to existing members or clients to gauge customer service quality.

- Consider if digital convenience or a personal touch matters more in your daily life.

- Think about where you’ll be banking long-term—relationship history can sometimes improve loan offers.

Legal, Regulatory, and Tax Considerations

Both banks and credit unions are overseen by strict national regulations. The FDIC and NCUA provide deposit security, and both must comply with anti-fraud and consumer privacy laws.

Tax implications of your loan, such as potential mortgage interest deductions, don’t vary based on where you borrow—but it’s best to confirm details with a tax professional or trusted resource.

Conclusion: Finding Your Best Fit

Credit unions and traditional banks both offer secure, regulated borrowing options. The best choice may boil down to your financial needs, preferred style of service, and eligibility.

Either way, understanding your own priorities helps. Hopefully, with a bit more clarity, choosing where to borrow becomes less daunting and even, perhaps, a little empowering.