A US credit statement is one of the most important documents tied to your card account, yet many people only look at the payment due and move on.

What most people actually need is a clear explanation of how a US credit statement works and what it tells you each month.

Once you know how to read it properly, you can catch mistakes faster, avoid unnecessary costs, and manage your account with more confidence.

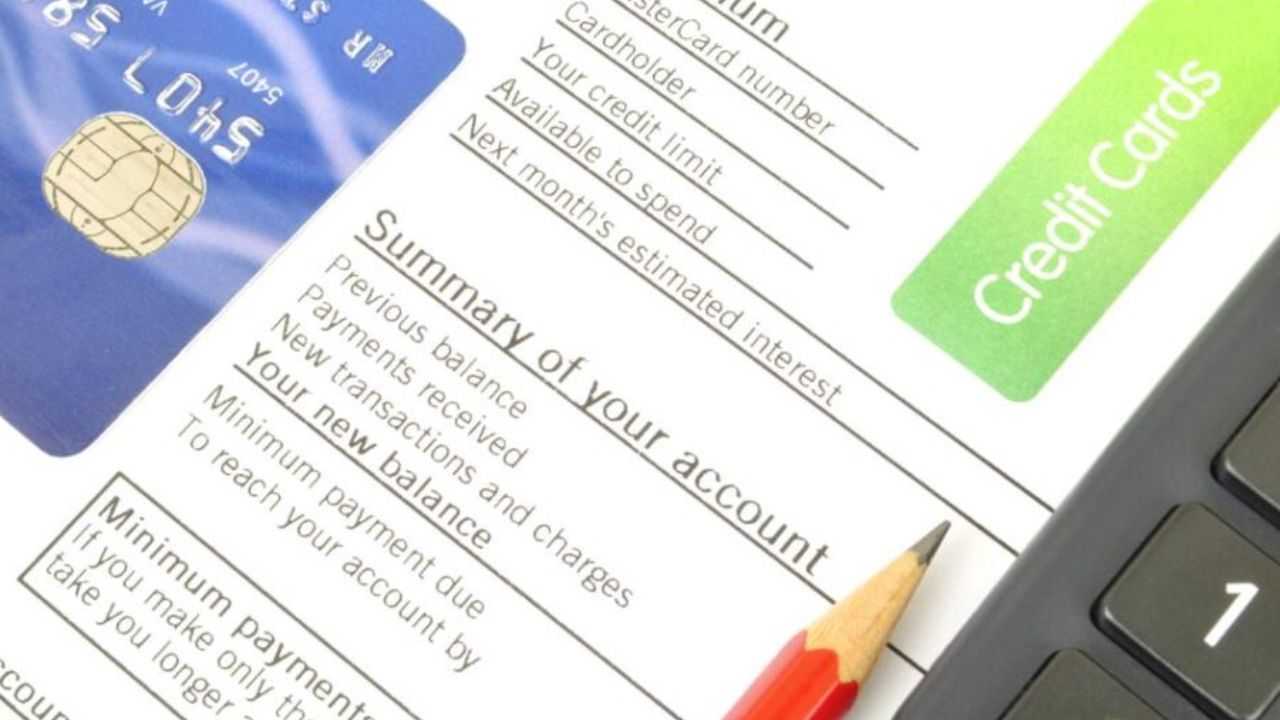

What A US Credit Statement Actually Shows

A US credit statement is your monthly summary of card activity during a specific billing cycle, and it shows how your balance changed from one period to the next.

It includes key details such as your previous balance, payments received, credits, purchases, fees, interest charges, new balance, minimum payment due, and payment deadline.

Most statements also show your available credit and may include notices about account terms or rate changes. When you read it carefully, the statement becomes more than a bill and starts to function as a practical financial record.

The Core Sections You See Every Month

Most credit statements follow a familiar structure even when the visual layout changes from one issuer to another.

You will usually see an account summary, a payment box, a transaction list, a section for fees and interest, and information about your credit limit or available credit.

Some statements also include promotional balance details, warning notices, or account messages that explain changes affecting your card. Knowing these sections makes it easier to read the document quickly without missing important information.

Why Statement Balance And Current Balance Are Not The Same

Many people confuse the statement balance with the current balance, but they do not mean the same thing.

The statement balance reflects what you owed at the end of the billing cycle, while the current balance may already include newer purchases, payments, or credits posted after the statement date.

That means the number printed on the statement is tied to a specific period, not necessarily the live amount showing in your app or online account. Reading the balance together with the statement date helps you understand what was actually billed for that cycle.

How To Read A Credit Statement Without Missing Important Details

The easiest way to read a credit statement is to follow the same order every month so you do not skip anything that affects what you owe.

Start with the most urgent details, then move into the sections that explain how the balance changed over the cycle.

This method keeps your review focused and makes it easier to notice suspicious charges, posting errors, or unexpected costs. A consistent routine also saves time because you know exactly where to look first.

Start With The Payment Box And Account Summary

Begin with the payment box because that section tells you the due date, the minimum payment, and the new balance, which are the most time-sensitive details on the page.

Once you confirm those numbers, move to the account summary to see how your previous balance changed through payments, credits, purchases, fees, and interest.

This gives you a fast overview of the billing cycle before you examine the details more closely. If the balance looks higher than expected, the summary usually points to the reason.

Review Transactions, Fees, Interest, And Credits Carefully

After reviewing the summary, go through the transaction list line by line and compare it with your receipts, order emails, subscription charges, or recent activity in your account history.

Check merchant names, dates, and amounts carefully because even small differences can point to a posting mistake or an unauthorized charge.

Then review any fees, finance charges, and credits to make sure everything was applied correctly. This step often reveals the problems people miss when they only look at the total due.

Common Mistakes And Warning Signs To Watch For

Credit statement errors are not always dramatic, and many are easy to miss because they show up as small charges, unfamiliar merchant names, or minor balance changes.

That is why it helps to review the statement as a record that needs checking, not just as a bill that needs payment.

When you look at it this way, inconsistencies become easier to spot before they turn into larger issues. A careful review each month can prevent avoidable fees, confusion, and account problems.

Charges That Do Not Look Familiar

One of the clearest warning signs is a charge you do not recognize, whether it is an unauthorized transaction, a duplicate entry, a strange merchant name, or a refund that never appeared.

In some cases, the billing name may differ from the brand you expected, so comparing the amount and date is just as important as reading the merchant line.

Small charges also deserve attention because they can sometimes be test transactions linked to fraud. If something still does not make sense after checking your records, it should be treated as a real issue.

Terms And Numbers That Signal A Possible Problem

Not every problem appears in the list of purchases, because some of the most important warning signs come from unexpected fees, unusual interest charges, missing credits, or changes in APR.

These details can quietly raise your balance over time, especially if they repeat across multiple statements.

You should also watch for payment posting problems or due date changes that do not match what you expected. A statement should explain your account costs clearly, so unexplained changes should never be ignored.

What To Do If You Find A Mistake On Your Statement

If you find a possible error, the best response is to act quickly and stay organized so the issue does not become harder to prove later.

Start by comparing the statement with your own records, including receipts, confirmation emails, cancellation notices, or refund messages.

Once you know exactly what looks wrong, contact the card issuer and document every step you take. Moving quickly gives you a better chance of resolving the issue cleanly and protecting your account.

How To Dispute A Billing Error The Right Way

When you dispute a billing error, clear documentation matters as much as the complaint itself.

Gather copies of any evidence that supports your claim, then explain the issue in a specific and direct way so the issuer can understand what needs to be reviewed.

Keep notes of phone calls, save emails, and keep copies of anything you send or receive during the process. A written dispute is especially useful because it creates a record that is much stronger than relying on memory alone.

When You Also Need To Check Your Credit Report

Some statement problems stay limited to one billing cycle, but others may affect your credit report if they involve payment status, account balances, or inaccurate reporting.

If the mistake is serious enough to affect how the account appears beyond the statement itself, checking your credit report becomes an important next step.

A corrected billing issue does not always mean the reporting side was updated properly. Looking at both the statement and the credit file gives you a more complete way to protect yourself.

Smart Habits That Help You Catch Problems Early

The easiest way to deal with statement problems is to build simple habits that help you catch them early and reduce confusion each month.

You do not need a complicated system, but you do need a routine that keeps your records clear and your review process consistent.

When statement checking becomes part of your monthly schedule, it takes less time and feels far less stressful. Prevention is usually easier than fixing a problem after it has already affected your balance or account history.

The Best Monthly Statement Review Routine

A strong review routine starts as soon as the statement becomes available instead of waiting until the due date is close. First, check the due date and minimum payment, then scan the account summary to see how the balance changed during the cycle.

After that, compare the transaction list with your purchases, subscriptions, refunds, and recent payments, then finish by checking fees, interest charges, and credits. Following the same order every month makes unusual activity easier to spot.

Tips That Help You Avoid Fees, Fraud, And Confusion

A few practical habits can make statement review much easier and much more accurate over time.

Save digital receipts for larger purchases, keep cancellation confirmations, and make sure you recognize the billing names used by subscriptions and online services.

It also helps to read account notices instead of skipping them, since changes to fees or rates may be explained there before they show up in your balance. Most importantly, do not rely only on memory, because your statement is a financial record that deserves a careful review.

Conclusion

A US credit statement becomes much easier to manage once you understand what each section is trying to show you and how the numbers connect. Instead of treating it as just another monthly bill, you can use it to track spending, verify charges, and catch mistakes before they turn into bigger problems.

When you review it in a consistent order and respond quickly to anything that looks wrong, you protect both your money and your account. That habit does not take long, but it can save you stress, confusion, and avoidable costs.